Overview

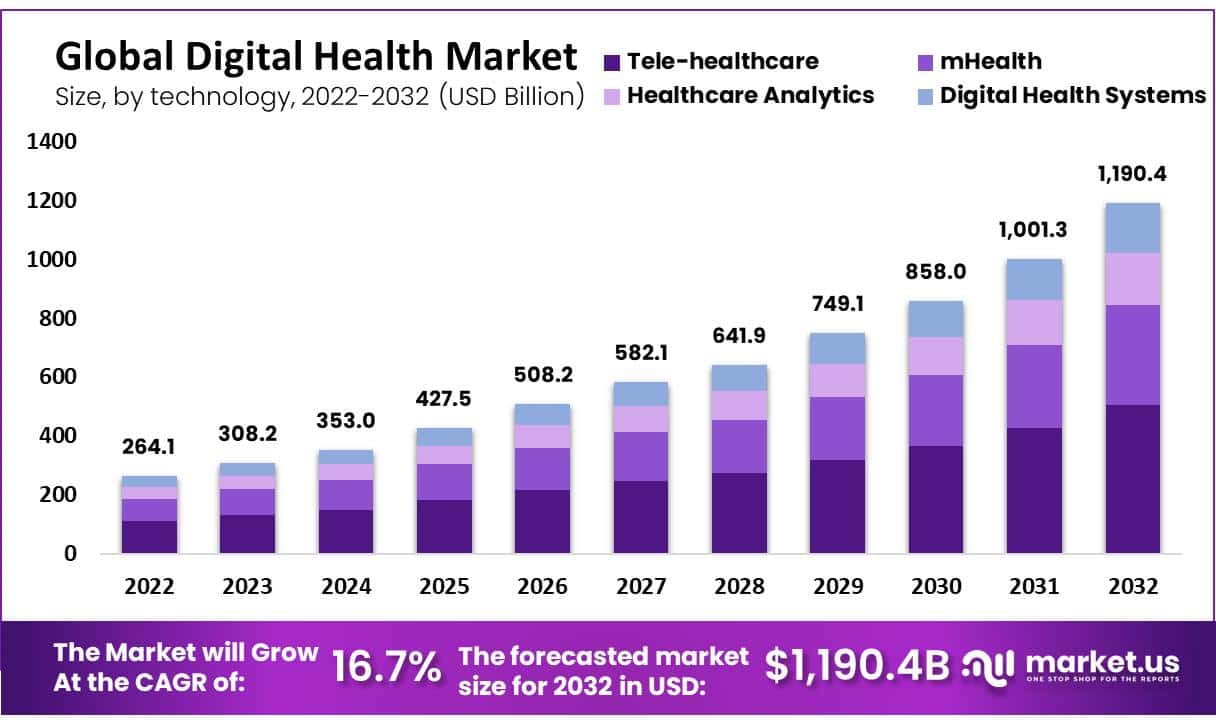

The Global Digital Health Market is projected to reach USD 1,190.4 billion by 2032, rising from USD 264.1 billion in 2022. This growth is expected at a CAGR of 16.7% from 2023 to 2032. The market expansion is driven by the increasing adoption of smartphones, high-speed internet access, and telehealth services. Improved healthcare IT infrastructure and rising chronic disease cases further support growth. Strategic collaborations, such as Teladoc Health’s integration with Microsoft Teams, are enhancing user access to virtual care, thereby accelerating market penetration globally.

Governments worldwide are implementing digital health programs to support infrastructure. India’s Ayushman Bharat Digital Health Mission and France’s US$ 650 million investment in digital health are key examples. The shortage of medical professionals in many countries is intensifying the need for remote healthcare. WHO estimates a shortfall of 15 million healthcare workers by 2030. Additionally, the aging population, expected to reach 1.5 billion by 2050, is increasing the demand for remote health solutions, supporting the growth of digital healthcare and telemedicine adoption.

Digital transformation is also driven by public awareness and the proliferation of health-focused mobile apps. As of 2022, over 6.6 billion smartphone users were online. Wearables and health apps are widely adopted due to rising interest in physical and mental well-being. In India, nearly 40% of people are willing to spend more on health-promoting products. Companies are responding by developing diverse health applications, with over 350,000 healthcare-related apps available globally. This trend is expected to continue due to strong digital engagement and AI innovations.

Despite strong growth, data privacy and cybersecurity remain major challenges. Health systems face increasing cyber threats, with over 239 million hacking attempts recorded in 2020 by the Health Sector Cybersecurity Coordination Center. Breaches of sensitive medical information, as reported by the HIPAA Journal, have raised concerns about patient data protection. Healthcare providers face difficulty in sharing data securely while ensuring compliance with privacy regulations. These issues may slow the digital health market’s growth if not addressed through robust data protection policies and systems.

Key Takeaways

- The global digital health market is projected to reach USD 1,190.4 billion by 2032, up from USD 308.2 billion in 2023.

- The market is expanding at a strong CAGR of 16.7% between 2023 and 2032, reflecting accelerated adoption of digital technologies across healthcare sectors.

- Telehealthcare remains the leading technology within digital health, accounting for approximately 42.5% of total revenue share due to its widespread clinical integration.

- Services dominate the digital health component segment, holding a 44.5% revenue share, driven by growing demand for remote monitoring and virtual consultations.

- Among end users, healthcare providers emerged as the primary adopters of digital health solutions, driven by the need for efficient care delivery systems.

- North America led regional performance in 2022, capturing 45.3% of the market share due to advanced infrastructure and favorable regulatory support.

- Rising venture capital investments in digital health startups highlight increasing innovation and strong investor confidence in the market’s long-term potential.

- Growing consumer demand for personalized, accessible healthcare is encouraging providers to implement digital tools that enhance patient engagement and convenience.

Regional Analysis

In 2022, North America led the digital health market with a 45.3% revenue share. The region was an early adopter of smart healthcare technologies, including wearables and mobile health apps. This was driven by high smartphone usage, improved network coverage, and rising chronic disease prevalence among the aging population. Additional contributors include increasing healthcare costs, caregiver shortages, and a growing need for chronic disease management. These combined factors have positioned North America as the dominant region in the digital health landscape during the reported period.

Asia Pacific is projected to witness the fastest growth rate throughout the forecast period. This surge is fueled by expanding adoption of eHealth platforms and rising healthcare expenditure across countries. Governments are actively promoting telehealth initiatives and remote patient monitoring solutions. World Bank data highlights healthcare spending in 2019 at 5.4% for China, 3.1% for India, and 10.7% for Japan. As digital infrastructure strengthens, global market leaders are increasingly investing in Asia Pacific’s rapidly evolving digital health ecosystem.

Segmentation Analysis

The global digital health market is segmented by technology into Telehealthcare, mHealth, Healthcare Analytics, and Digital Health Systems. Telehealthcare led the segment with a 42.5% revenue share, driven by rising demand for real-time monitoring, population health management, and secure data storage. Technological advancements, especially disease-monitoring platforms, continue to fuel adoption. For example, GlobalMed introduced its Transportable Audiology Backpack in 2022 to support remote audiology care. With rising chronic conditions and growing elderly populations, this segment is expected to grow at a CAGR of 22.5% during the forecast period.

By component, the digital health market includes Software, Hardware, and Services. The services segment accounted for the highest revenue share at 44.5%, owing to growing demand for training, maintenance, and technical support. The availability of pre- and post-installation services by key providers enhances adoption. Meanwhile, the software segment is projected to grow at the fastest CAGR of 17.9%, due to rising demand from hospitals, patients, and insurers. Integration of AI, deep learning, and remote analytics functionalities in digital health solutions continues to drive software deployment.

In terms of end users, the market is divided into Healthcare Providers, Payers, and Healthcare Consumers. In 2022, healthcare providers dominated the segment due to a rising burden of chronic diseases and increasing use of mHealth applications. This trend is likely to continue through the forecast period. Payers are also witnessing strong growth, supported by the surge in healthcare IT adoption to manage rising medical costs and optimize patient engagement solutions.

Get Sample: https://market.us/report/digital-health-market/request-sample/

Key Players Analysis

Competition in the digital health market is growing rapidly due to the sector’s increasing digitalization. Leading companies are launching advanced telehealth platforms to gain a competitive edge. For example, American Well introduced its Converge platform in April 2021. This platform enhances connectivity among stakeholders and meets the rising demand for remote medical services. Telehealth technologies are now widely used to support healthcare professionals, which is intensifying competition across regions. The push for innovation is reshaping the digital healthcare landscape and accelerating platform deployment globally.

The market remains highly fragmented, with numerous local and regional players active across different segments. Major players with strong brand presence and robust distribution networks have a competitive advantage. These firms are implementing growth strategies like partnerships, collaborations, and product launches to maintain their market positions. The presence of both established and emerging companies creates a dynamic and fast-evolving environment. Continuous technological upgrades and user-focused digital health solutions are key to surviving in this space.

Key companies shaping the digital health sector include BioTelemetry Inc., eClinicalWorks, and Allscripts Healthcare Solutions Inc. Other significant players are iHealth Lab Inc., AT&T, and Honeywell International Inc. Firms like Athenahealth Inc., Cisco Systems, McKesson Corporation, Koninklijke Philips N.V., AdvancedMD Inc., and Cerner Corporation also hold strong positions. Together, these companies are advancing digital health innovation and expanding their global market share. Many other regional firms contribute to the competitive ecosystem.

Conclusion

In conclusion, the digital health market is growing quickly due to rising use of smart devices, better internet access, and strong public interest in virtual care. Healthcare providers are adopting digital tools to manage patient care more efficiently and reach people in remote areas. Governments are also supporting this shift through national programs and investments. While digital health offers many benefits, privacy and data protection challenges must be addressed. As more people rely on mobile apps and wearable devices, companies are creating advanced solutions to meet changing needs. With ongoing innovation and global support, digital health is expected to remain a key part of future healthcare systems.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Wearable Sleep Trackers Market

IVF Devices And Consumables Market