Every few years the roster of top value creators reshuffles. The easy lesson one may take writes itself: pick the right industry at the right moment, and the returns follow. BCG’s 2026 Value Creators rankings just delivered a fresh version of that story, but there is a far more useful one buried underneath it.

On the surface, the headline is rotation. After a decade in which technology-driven sectors owned the top of the table, asset-heavy industries such as mining, oil and gas, aerospace and defense, construction, banking have climbed into the lead. The most jarring move is in the other direction: software and IT services, a top-five sector last year, fell roughly twenty-seven places into the bottom of the pack.

The drivers are real and structural as AI’s first wave is rewarding the physical infrastructure layer of chips, power, and data centers; capital is rotating toward tangible assets; higher rates have lifted the banks. Markets have stayed strong through all of it, returning around twelve percent a year since 2020, with eleven companies now worth more than a trillion dollars. While most people will read those rankings as a sector story, value creators read them differently.

The Rotation Everyone Will Misread

The temptation is to treat the leaderboard as a map: be in the favored sectors, avoid the falling ones, and let the tide carry you. It’s a comfortable story because it’s the one that lets a leadership team off the hook. The sector did it, the macro did it, the rates did it. We were powerless.

Yet the same BCG dataset quietly dismantles that reading. In all but three of the thirty-five industries studied, the top-quartile companies beat the twelve-percent market median including industries sitting near the bottom of the overall rankings. A company in a “losing” sector routinely outperformed, while a company in a “winning” sector routinely didn’t. BCG’s own phrase for it is blunt: industry is not destiny.

That single finding reframes everything: the macro environment sets the terrain, it does not pick the winner.

Why Industry Is Not Destiny for Value Creators

Here’s the part the rankings can’t show you on their own: if sector doesn’t separate the value creators from the also-rans, something else must. And it turns out we have unusually clean evidence for what that something is.

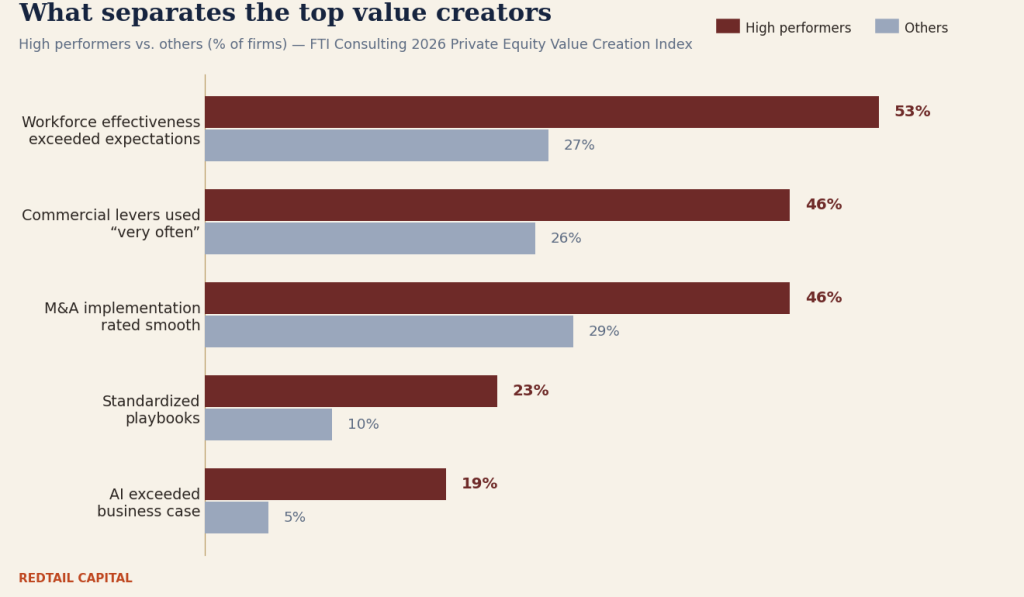

FTI Consulting’s 2026 Private Equity Value Creation Index surveyed more than 550 senior private equity leaders and did something most studies don’t. It isolated the roughly forty percent of firms whose portfolio companies consistently exceed their business case, and asked what those high performers do that everyone else doesn’t. The PE context is a useful microscope here, because private equity strips the question down to its bones. When you can no longer buy cheap and lever up, value has to be built from the inside out. There’s nowhere for sector luck to hide.

The behaviors that separated the winners weren’t sector-specific. They were system-specific:

- They get more from their people. High performers exceeded expectations on workforce effectiveness at nearly twice the rate of their peers — the widest gap of any lever in the survey. They develop the team they have instead of defaulting to reshuffling the org chart.

- They run commercial levers harder. Pricing, sales effectiveness, market expansion, customer retention — deployed at roughly twice the frequency of everyone else, and started in diligence rather than bolted on later.

- They execute M&A with discipline. The gap isn’t in sourcing deals; it’s in post-close execution and staying true to the original thesis as the deal evolves.

- They institutionalize the playbook. High performers are 2.3x more likely to run standardized playbooks — not because the document is magic, but because it encodes the know-how to execute fast and consistently.

- They treat AI as an amplifier, not an initiative. Adoption rates are similar across the board. What differs is application: high performers were nearly four times as likely to beat their AI business case, because they aimed it at a few high-leverage levers and tied each use case to a P&L line.

Read that list again and notice what’s missing. Not one of those advantages depends on being in the right industry. As one of the report’s authors put it, what sets the leaders apart is an activist approach to value creation, not a passive one. Diagnose honestly, plan against the thesis, execute relentlessly and reassess. The terrain changes; the discipline doesn’t.

Value Leaks by System, Not by Sector

If that’s how value gets built, it’s worth being just as precise about how it gets lost, because the two are the same mechanism running in reverse.

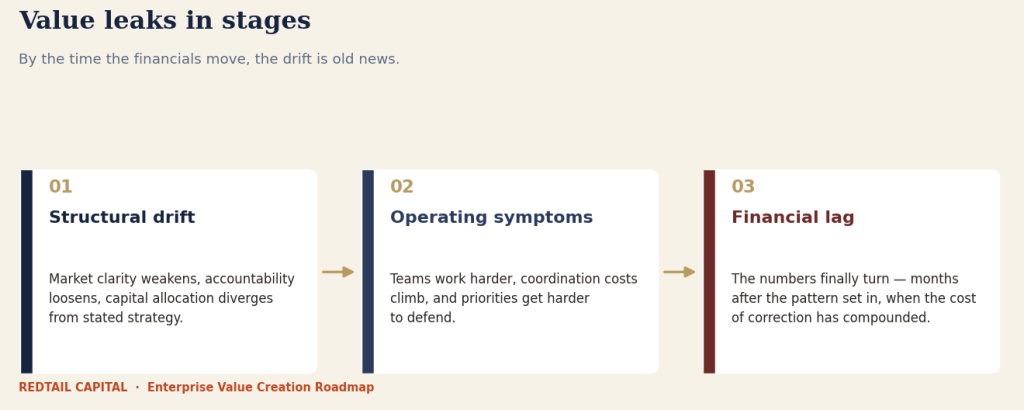

Value rarely leaks all at once. It leaks in stages. First comes structural drift: market clarity weakens, accountability loosens, capital allocation quietly diverges from stated strategy. Then the operating symptoms spread as teams work harder, coordination costs climb, and priorities get harder to defend. Only at the end does the financial lag appear, by which point the pattern has been forming for months and the cost of correcting it has compounded. It’s the arc we traced through the Stellantis turnaround story: the financials were the last thing to break, not the first.

This is the blind spot in the way most companies watch themselves. Dashboards, KPI reports, and quarterly reviews are built to observe outcomes against targets. They are not built to diagnose the structural conditions that produce those outcomes. By the time a number turns red, the drift is old news. Value creators look below the surface and identify areas of focus before the reports come out.

The FTI data shows the cost of that lag in real time. Speed-to-value has become the differentiator: sixty-three percent of firms now expect a lever to deliver inside twelve months, up from forty-one percent a year ago. Execution, meanwhile, is the universal weak point. M&A, which vaulted from the lowest-priority lever to the highest in a single year, is rated as running smoothly by barely a third of firms. The returns are there for those who get execution right; fifty-one percent are beating their M&A business case. The gap between those two numbers is the whole game.

And the market is no longer paying for promises. For U.S. non-financial companies, the gap between price and underlying fundamentals, BCG calls it “expectation premium,” has reached its highest level since 1926, higher even than the peak of the dot-com bubble. When expectations are priced that richly, the only durable answer is fundamental: real margin, real growth, real operational proof. PE buyers have already drawn the same conclusion. Margin expansion and operational efficiency is now the number-one factor they look for at exit, while “AI-ready” as a standalone selling point collapsed from the top of the list to near the bottom. Buyers stopped buying the story, they want it embedded in the results.

Bring the Whole System (and the Investors) Along

There’s a final thread that runs through both reports, and it’s the one we keep coming back to: nobody creates durable value alone.

BCG is direct that the quality of a company’s investor base is itself a strategic asset. Make the right calls but fail to bring investors along, and the choices never show up in the valuation. FTI’s high performers tell the same story from the operating side: they embed operating partners alongside management, align incentives, and build the exit narrative from day one rather than assembling it in a panic in the final year. Strategy, capital, people, and the people backing the capital all have to be pulling the same direction. If the partners, the team, and the investors don’t win together, the value doesn’t hold. Alignment isn’t a soft virtue here, it’s the load-bearing structure.

That’s the reason industry is not destiny. A sector is a circumstance, but a business system is a choice, and an interconnected one at that. Value doesn’t accrue to the company in the best neighborhood. It accrues to the company that can see its whole system clearly, decide what to fix first, and execute before the financial lag forces its hand.

Which is exactly the problem the Enterprise Value Creation Roadmap was built to solve. It reveals where value is being created or eroded across the full business system, external, internal, and financial, and shows leaders the structural conditions behind the numbers before those conditions reach the income statement. It models the terrain so the team can choose the road.

The market may sort the sectors, but discipline sorts the companies. The value creators who lead the next cycle won’t be the ones who happened to be standing in the right industry when the tide came in. They’ll be the ones who did the work that the tide can’t do for you.