In today’s interconnected economy, more individuals and businesses are handling transactions in multiple currencies. Whether it’s a freelancer billing clients abroad, a small e-commerce shop selling to international customers, or a traveler managing expenses overseas, the need for efficient and cost-effective currency solutions has never been greater.

One way people are meeting this need is by using multi-currency accounts. These accounts provide a centralized place to hold, send, and receive different currencies without requiring separate accounts in each country.

What Is a Multi-Currency Account?

A multi-currency account functions like a standard bank account, but it can hold balances in more than one currency at a time. Instead of maintaining several accounts in various countries, users can store, convert, and manage foreign currencies in one place.

These accounts are offered by both traditional banks and newer fintech services. They can be accessed through physical branches, online platforms, or mobile apps, making them convenient for different types of users.

Key Advantages

1. Reduced Currency Conversion Costs

When sending or receiving money internationally through a standard bank account, transactions often involve converting one currency into another. This conversion typically comes with fees or less favorable exchange rates. Multi-currency accounts allow users to hold funds in the currency of their choice, which can help avoid repeated conversions and associated costs.

2. Faster Transactions

Holding funds in the currency of the destination country can speed up transfers. Payments can be made directly in the required currency, reducing the processing time that banks often need for conversion.

3. Simplified Record-Keeping

For businesses, maintaining multiple ledgers for different currencies can be time-consuming. A multi-currency account consolidates these transactions, making it easier to track income and expenses across markets.

4. Greater Financial Flexibility

Individuals who travel frequently or relocate abroad benefit from being able to access different currencies instantly. This flexibility can be especially useful in volatile exchange rate environments.

Who Benefits Most?

Multi-currency accounts are not just for large corporations. They can be a practical solution for:

Freelancers who work with clients worldwide and receive payments in multiple currencies.

Small businesses selling goods or services internationally.

Frequent travelers who want to avoid high foreign transaction fees.

Remote workers living in one country while being paid from another.

Security and Compliance Considerations

While multi-currency accounts offer convenience, it’s important to choose a provider that prioritizes security. Look for accounts that include encryption, two-factor authentication, and fraud detection systems.

It’s also essential to ensure that the account provider complies with financial regulations in the relevant jurisdictions. This not only protects the user but also ensures smooth cross-border transactions without regulatory complications.

Digital Platforms Offering Multi-Currency Services

The rise of fintech has made multi-currency accounts more accessible. Digital platforms are streamlining international transactions, often with lower fees and better user experiences compared to traditional banks.

For example, the blackcat website provides information on services that combine payment flexibility with modern financial tools, enabling users to manage various currencies and transactions from a single interface.

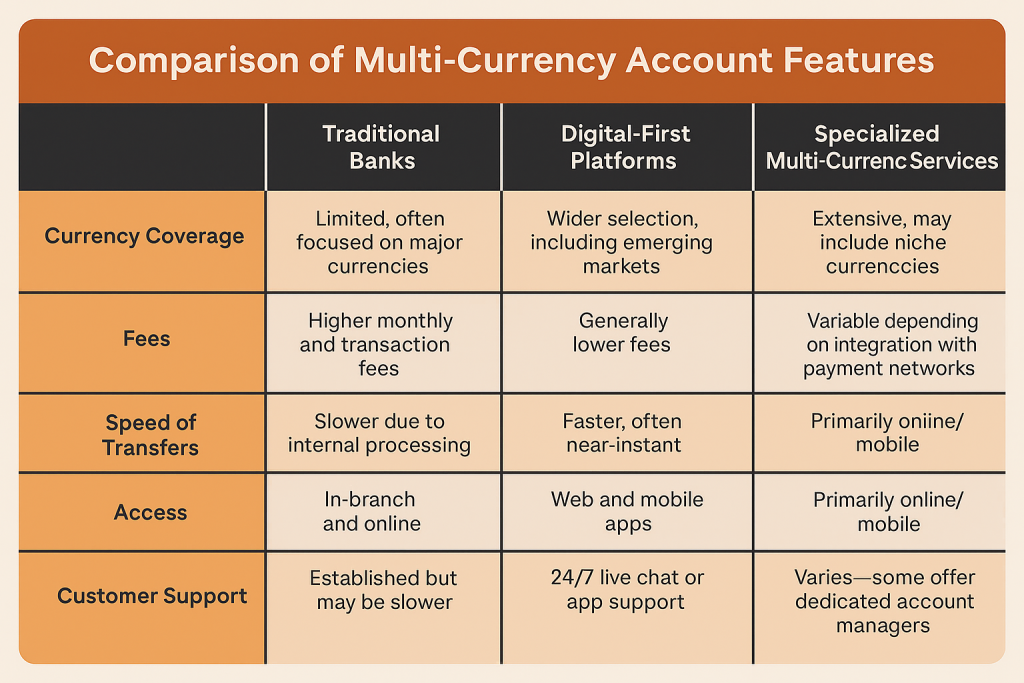

Comparison of Multi-Currency Account Features

| Feature | Traditional Banks | Digital-First Platforms | Specialized Multi-Currency Services |

|---|---|---|---|

| Currency Coverage | Limited, often focused on major currencies | Wider selection, including emerging markets | Extensive, may include niche currencies |

| Fees | Higher monthly and transaction fees | Generally lower fees | Competitive, but may charge for premium features |

| Speed of Transfers | Slower due to internal processing | Faster, often near-instant | Variable depending on integration with payment networks |

| Access | In-branch and online | Web and mobile apps | Primarily online/mobile |

| Integration | Limited for business tools | Good integration with e-commerce and accounting | Designed with cross-border business in mind |

| Customer Support | Established but may be slower | 24/7 live chat or app support | Varies—some offer dedicated account managers |

Potential Drawbacks

Maintenance fees on some accounts.

Currency limits for supported balances.

Exchange rate fluctuations that can affect stored balances.

How to Choose the Right Account

When evaluating providers, consider:

Currency coverage – Does the account support the specific currencies you need?

Fee structure – Are there monthly fees, and what are the transaction charges?

Ease of use – Is there a user-friendly web or mobile platform?

Integration options – For businesses, can it connect with accounting or e-commerce systems?

Customer support – Is assistance available in your time zone and language?

The Future of Multi-Currency Banking

With global commerce continuing to expand, demand for flexible currency management will only increase. Fintech innovation is likely to introduce even more features, such as instant currency swaps, integrated payment solutions, and AI-driven tools for optimizing transactions.

As technology evolves, the distinction between domestic and international banking is becoming less pronounced. Multi-currency accounts are at the forefront of this shift, offering a practical way for people and businesses to manage finances in a globalized world.