Overview

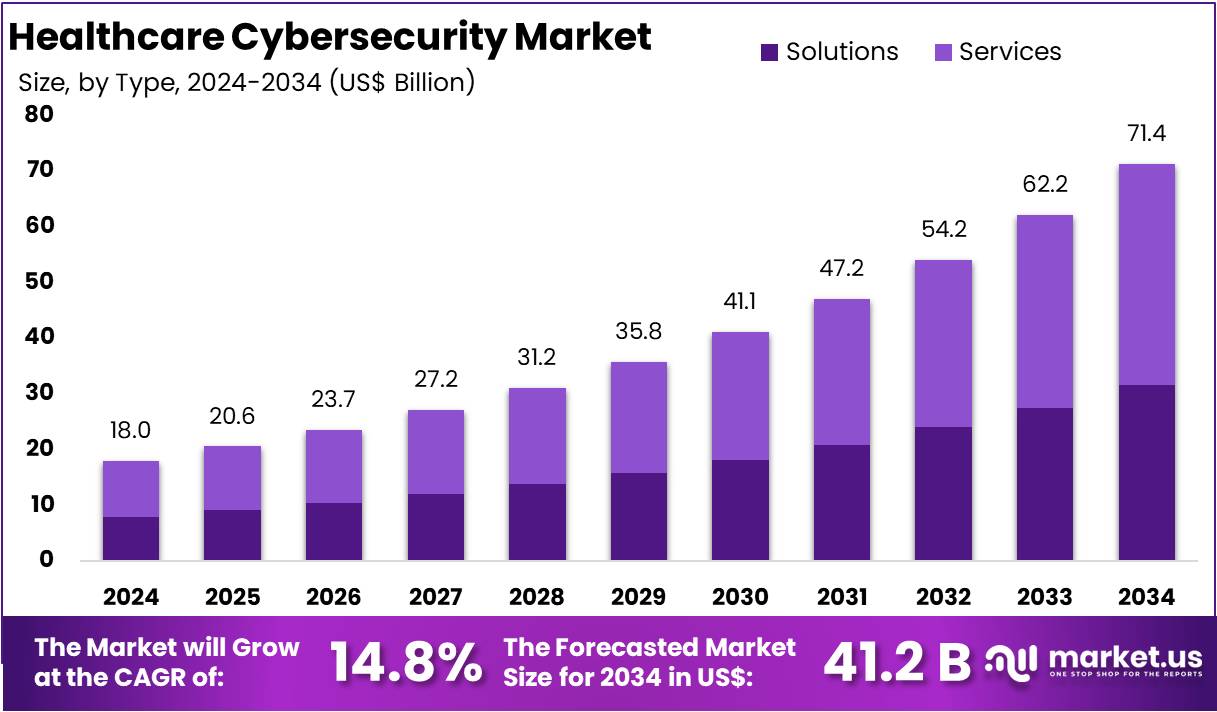

The Healthcare Cybersecurity Market is projected to reach approximately USD 71.36 billion by 2034, rising from USD 17.95 billion in 2024. This growth is expected at a CAGR of 14.8% from 2025 to 2034. The market focuses on cybersecurity solutions designed to protect healthcare data and digital systems. Growth is driven by increasing cyber threats, rising adoption of healthcare IT, and heightened regulatory standards. As digital transformation continues, the demand for advanced security measures across healthcare systems is expected to intensify steadily.

Healthcare remains one of the most targeted industries for cyberattacks. As of January 2022, the U.S. Department of Health and Human Services (HHS) reported 860 major data breaches involving protected health information. Among these, 119 breaches were linked to third-party vendors or business associates. A single breach affected 3.25 million individuals. According to IBM and the Ponemon Institute, the average cost of a healthcare breach stood at USD 9.23 million, more than double the average across all sectors, reflecting the critical need for robust cybersecurity systems.

The market includes a range of cybersecurity solutions such as network security, cloud security, endpoint protection, and application security. These services are offered by general cybersecurity providers, healthcare-specific vendors, and IT solution companies. The increasing demand for cloud-based security is a key trend, especially in light of growing data volumes and mobile access requirements. As healthcare data becomes more digitized, organizations must invest in scalable and secure systems that meet evolving regulatory and operational demands.

A sharp rise in healthcare-related cyber incidents is fueling market growth. In 2023 alone, over 93 million patient records were breached from business associates, outpacing the 34.9 million records compromised at provider level. Hacking-related breaches rose by 239% from 2018 to 2023, while ransomware attacks increased by 278%. The share of hacking incidents grew from 49% in 2019 to 79.7% in 2023. These statistics highlight the urgency for healthcare institutions to enhance digital protection mechanisms.

Government policies and global data protection laws are further propelling the market. Regulations such as HIPAA in the U.S. and GDPR in the EU are compelling healthcare providers to adopt strict cybersecurity frameworks. The widespread use of connected devices and telehealth systems since the COVID-19 pandemic has increased system vulnerabilities. This rising digital dependency has reinforced the need for comprehensive endpoint and network security solutions. Consequently, regulatory enforcement, paired with digital growth, is driving strong momentum across the healthcare cybersecurity market.

Key Takeaways

- In 2024, the global healthcare cybersecurity market generated approximately US$ 95 billion in revenue, with projections estimating it will reach US$ 71.36 billion by 2034.

- The market expanded at a robust CAGR of 14.8%, driven by increasing cyber threats and digital transformation within the global healthcare ecosystem.

- Among product types, services held a dominant position in 2024, capturing 55.6% of the overall market share across global healthcare cybersecurity solutions.

- Within solution types, Identity and Access Management (IAM) led the market in 2024, accounting for 19.7% of total solution-based revenues.

- Malware emerged as the leading cyber threat category, contributing 25.9% to the total market share in the threat-based segmentation.

- Network Security dominated the security segment in 2024, securing 30.5% of the market share as institutions prioritized infrastructure protection.

- On-Premises deployment led the market with 56.8% share in 2024, as many healthcare institutions preferred direct control over data environments.

- Hospitals were the largest end-users of healthcare cybersecurity in 2024, generating 40.2% of the sector’s total revenue share.

- Geographically, North America led the global market in 2023, accounting for 30% of total revenue due to high digital healthcare adoption.

Get Sample: https://market.us/report/healthcare-cybersecurity-market/request-sample/

Regional Analysis

The North American healthcare cybersecurity market is expanding rapidly. This growth is driven by the increasing number of cyber threats targeting healthcare systems. Frequent attacks such as ransomware and data breaches are creating high demand for advanced cybersecurity tools. These threats compromise sensitive patient information. As a result, healthcare providers are prioritizing security investments. The rising need to safeguard electronic health records and digital platforms is pushing the market forward. Cybersecurity has become a critical part of digital infrastructure in the region’s healthcare sector.

Regulatory mandates are also fueling market growth. Laws such as the Health Insurance Portability and Accountability Act (HIPAA) require strict data protection standards. These regulations compel healthcare organizations to implement comprehensive cybersecurity frameworks. Non-compliance can lead to financial penalties and reputational damage. Consequently, healthcare entities are adopting advanced systems to meet legal requirements. These efforts are strengthening cybersecurity adoption across the region. Regulatory compliance remains a key factor in shaping market dynamics in North America.

The digital transformation in healthcare is another significant contributor. Hospitals and clinics are embracing electronic health records (EHRs), telehealth platforms, and Internet of Medical Things (IoMT) devices. While these technologies enhance efficiency, they also increase the risk of cyberattacks. Each connected system presents a potential entry point for hackers. This expanded digital landscape has made robust cybersecurity solutions indispensable. Healthcare providers are investing in multi-layered security to manage new digital risks effectively.

Emerging trends are shaping the future of this market. Cloud-based security solutions are gaining popularity due to their scalability and cost-efficiency. Artificial intelligence (AI) and machine learning (ML) are being deployed for faster threat detection and response. The Zero Trust architecture model is being widely adopted to limit internal and external access risks. These innovations are improving the sector’s cyber resilience. North America is expected to maintain its leadership position as healthcare organizations continue prioritizing data protection and compliance.

Segmentation Analysis

In 2024, the Services segment dominated the healthcare cybersecurity market with a 55.6% share. This growth is driven by rising demand for managed security services. Healthcare organizations rely on external firms for 24/7 threat monitoring, incident response, and regulatory compliance. Security-as-a-Service (SECaaS) models are becoming essential for organizations lacking in-house expertise. As cyber threats grow in complexity, specialized services have become critical for effective protection. Outsourcing cybersecurity functions helps healthcare providers maintain system security and meet evolving data protection standards efficiently.

Among various solution types, Identity and Access Management (IAM) held the largest market share at 19.7% in 2024. IAM systems are essential for ensuring that only authorized users access sensitive patient data. Compliance requirements such as HIPAA have increased the need for secure access control. The adoption of electronic health records (EHRs) has further heightened demand for IAM tools. These tools enforce user authentication, role-based access, and activity monitoring. IAM plays a vital role in strengthening the digital security posture of healthcare institutions.

Malware emerged as the top cyber threat in 2024, accounting for 25.9% of the threat landscape in healthcare. Ransomware attacks are particularly damaging, locking critical systems and disrupting patient care. Cybercriminals exploit the urgency in healthcare to demand ransoms. As digital adoption increases, so does exposure to malware threats. Healthcare providers are focusing on prevention and rapid response strategies. Investment in anti-malware solutions and incident readiness has become a high priority to protect operational continuity and patient safety.

Network Security led the healthcare cybersecurity market by security type, capturing a 30.5% market share in 2024. The growing use of interconnected systems and medical devices increases the need for network defense. Firewalls, intrusion detection systems, and VPNs are widely adopted to prevent breaches. These tools protect healthcare networks from unauthorized access and data theft. With sensitive data flowing through multiple digital channels, strong network security remains a top priority for healthcare institutions aiming to avoid cyber incidents.

Cloud-based deployment held the dominant share of 56.8% in 2024. The shift to cloud computing in healthcare is driven by scalability and cost efficiency. Cloud deployments allow easy access to security tools without heavy infrastructure investment. Built-in features like encryption and multi-factor authentication enhance data security. Hospitals, which held 40.2% of the end-user market, rely heavily on these cloud systems. Hospitals face high cyber risk due to the volume of patient data. Thus, cloud solutions offer flexible, secure, and compliant data protection methods.

By Type

- Solutions

- Services

By Solution Type

- Identity and Access Management (IAM)

- Data Loss Prevention (DLP)

- Antivirus and Antimalware

- Log Management and SIEM

- Firewall

- Encryption and Tokenization

- Compliance and Policy Management

- Patch Management

- Others

By Threat

- Malware

- Advanced Persistent Threats (APT)

- Distributed Denial of Service (DDoS)

- Spyware

- Phishing

- Ransomware

- Others

By Security

- Network Security

- Endpoint Security

- Cloud Security

- Application Security

By Deployment Mode

- On-Premises

- Cloud-Based

By End-User

- Hospitals

- Pharmaceutical Companies

- Health Insurance Providers

- Clinical Laboratories

- Government Healthcare Agencies

- Research Institutions

- Telehealth and Digital Health Providers

Key Players Analysis

The healthcare cybersecurity market is driven by key players such as Symantec (Broadcom), Kaspersky, and Northrop Grumman. Symantec delivers robust cybersecurity products including endpoint and cloud security. These tools ensure regulatory compliance and protect sensitive patient data. Kaspersky offers antivirus and endpoint protection, focusing on threat detection and HIPAA compliance. Northrop Grumman supports secure infrastructure and data encryption for healthcare providers. These firms play a major role in securing healthcare IT networks and enabling safe digital transformation in the industry.

Other significant contributors include Palo Alto Networks, Fortinet, McAfee, and Cisco Systems. Palo Alto Networks specializes in firewall and threat prevention solutions. Fortinet provides integrated security across endpoints and cloud systems. McAfee offers advanced threat intelligence and endpoint security. Cisco Systems enhances network security with scalable, enterprise-grade solutions. These companies strengthen healthcare cybersecurity frameworks by delivering comprehensive, real-time protection against evolving cyber threats.

Additional players like Check Point Software Technologies, IBM, Trend Micro, and CrowdStrike also shape the market landscape. IBM offers AI-driven threat detection and security analytics. Trend Micro delivers cloud and hybrid environment protection. CrowdStrike focuses on endpoint protection and threat intelligence. Companies such as FireEye, NortonLifeLock, Barracuda Networks, Proofpoint, Sophos, Cloudflare, Microsoft, and other notable firms further expand the market. Together, these players ensure a resilient and secure healthcare infrastructure.

Conclusion

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More